Schedule a Demo

Schedule a Demo

Read More

Content

Filter

10 results found

Featured

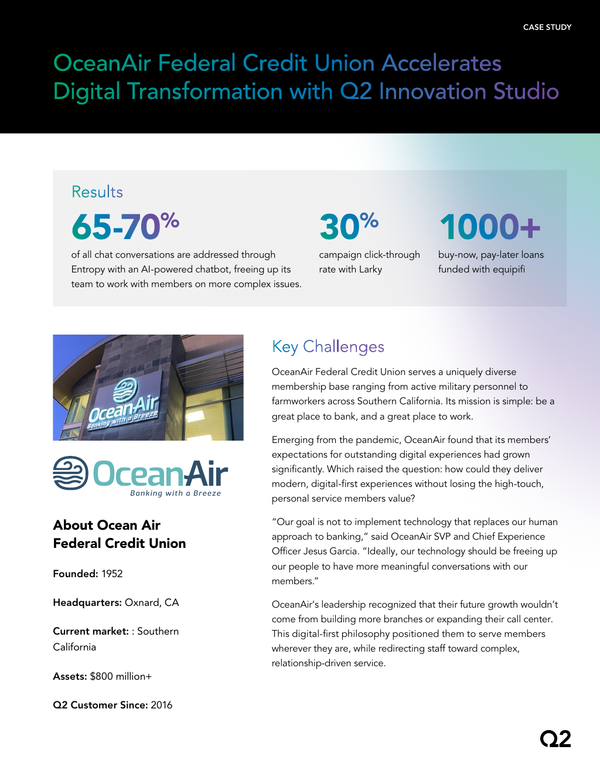

OceanAir Federal Credit Union Case Study

Featured

Gesa Credit Union Case Study

Featured

PeoplesBank Uses Education, Innovation to Protect Their Business Customers

Featured

Get the Latest News and Updates from Q2

Featured

Inside Gen Z: The Story Behind the Numbers

Featured

Fraud Intelligence: Build Trust. Not Friction (ebook)

Featured

Commercial Loan and Deposit Pricing Market Update: September 2025

Featured

Striking the Balance With Fraud Management

Featured

Lessons in Loyalty: A Live Q&A With Gen Z Consumers

Featured

Inside Gen Z: Lessons in Loyalty

Featured

Content types

None

Case Study

(1)

Blog

(3)

Podcast

(2)

White Paper

(1)

Webinar

(1)

Topics

None

Digital Banking

(6)

Fintech partnerships

(3)

Personalization

(3)

Fraud

(4)

Commercial Pricing

(1)

Money Movement

(1)

Segment

None

Consumer

(7)

Small Business

(5)

Commercial

(5)

Solutions

None

Digital Banking Platform

(5)

Personal Finance Management

(2)

Targeting and Marketing

(2)

Risk and Fraud

(3)

Relationship Pricing

(1)

Fintech Integration

(1)

Payments

(1)