Schedule a Demo

Schedule a Demo

Read More

Content

Filter

10 results found

Featured

Inside Digital Transformation: The Path From Evaluation to Innovation

Featured

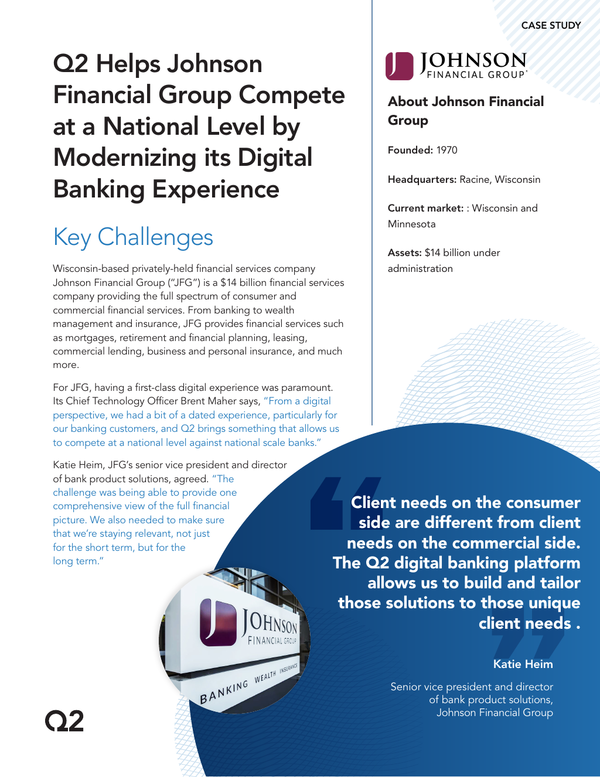

Johnson Financial Group Case Study

Featured

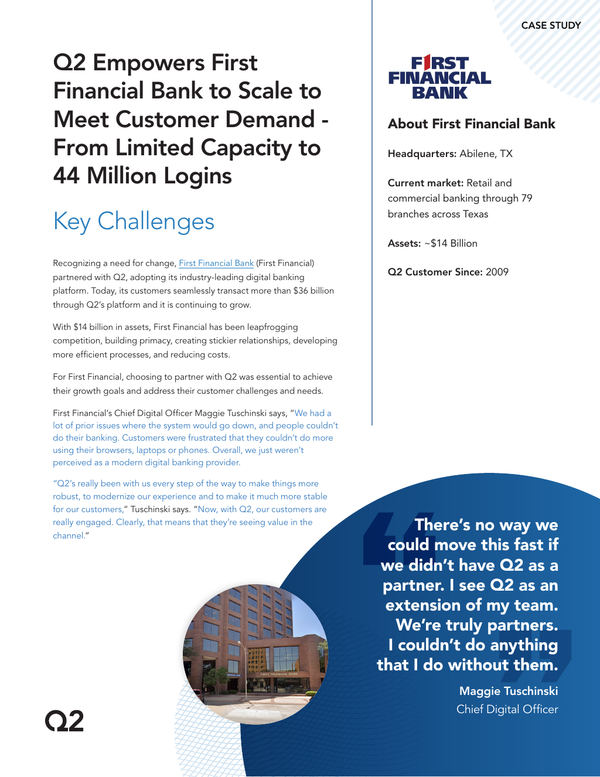

First Financial Bank Case Study

Featured

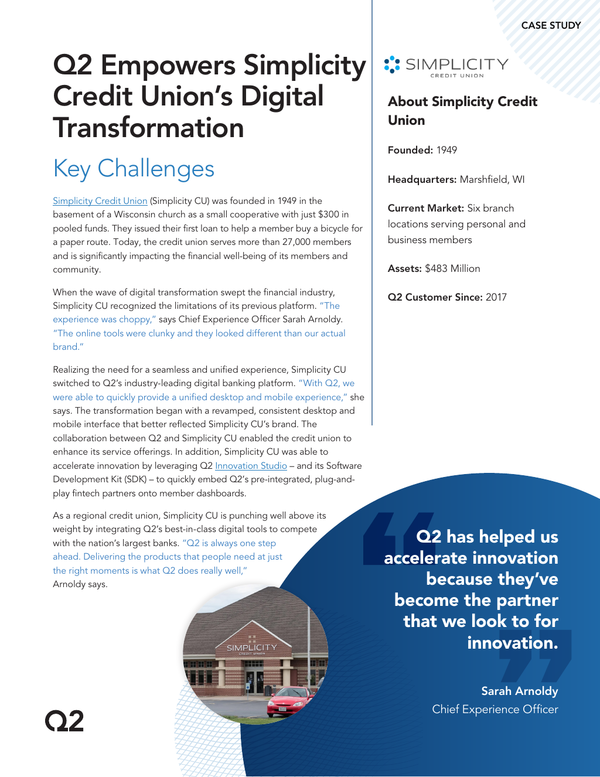

Simplicity Credit Union Case Study

Featured

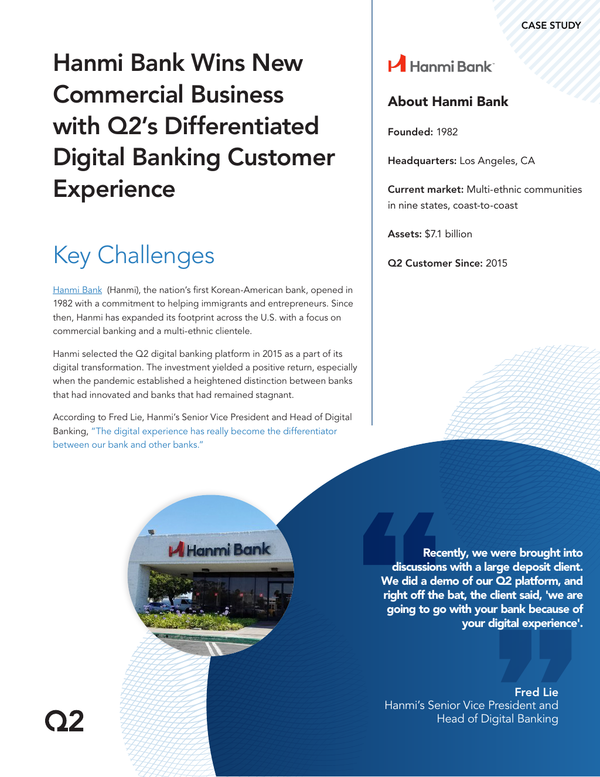

Hanmi Bank Case Study

Featured

2026 State of Commercial Banking

Featured

Can You Fight Fraud and Improve Customer Experience at the Same Time?

Featured

Q2 Caliper SDK

Featured

What High-Performing Banks Dare to Do Differently

Featured

Reg E in a Fraud-Heavy World: Turning Disputes into Trust

Featured

Content types

None

Webinar

(3)

Case Study

(2)

Podcast

(2)

Product Collateral

(1)

Topics

None

Digital Banking

(7)

Fintech partnerships

(5)

Personalization

(2)

Fraud

(4)

Positive Pay

(1)

AI

(1)

Money Movement

(1)

Commercial Pricing

(1)

Segment

None

Consumer

(7)

Small Business

(5)

Commercial

(6)

Solutions

None

Digital Banking Platform

(7)

Fintech Integration

(6)

Risk and Fraud

(4)

Relationship Pricing

(1)

Payments

(1)

Targeting and Marketing

(1)