Schedule a Demo

Schedule a Demo

Read More

Content

Filter

10 results found

Featured

Q2 Caliper SDK

Featured

What High-Performing Banks Dare to Do Differently

Featured

Reg E in a Fraud-Heavy World: Turning Disputes into Trust

Featured

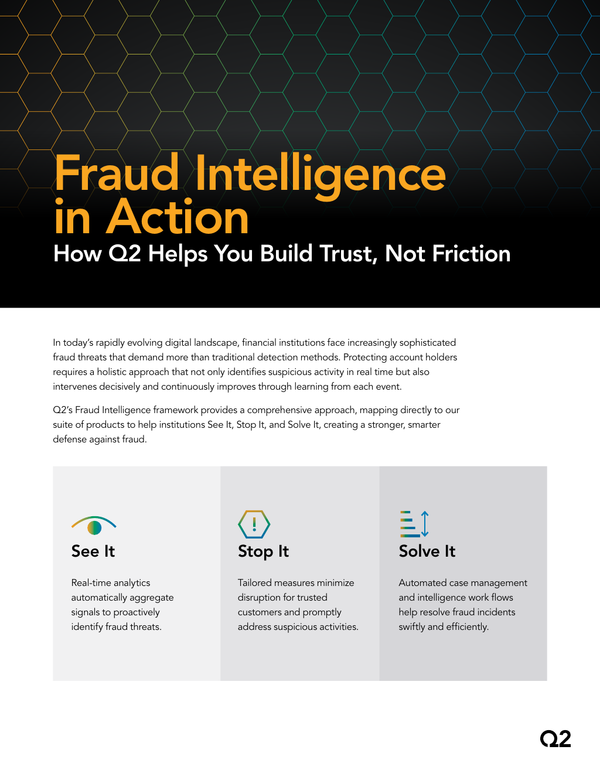

Fraud Intelligence in Action: How Q2 Helps You Build Trust, Not Friction

Featured

Art, Algorithms, and the Future of AI in Banking

Featured

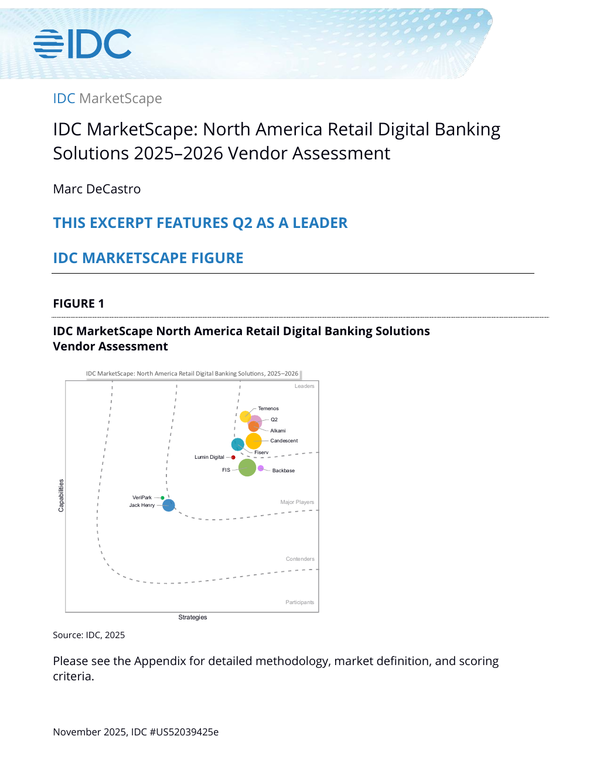

IDC MarketScape: North America Retail Digital Banking Solutions 2025-2026 Vendor Assessment

Featured

Q2 Engage Personalization Tools Solution Brief

Featured

Lessons From America's Top-Performing Banks

Featured

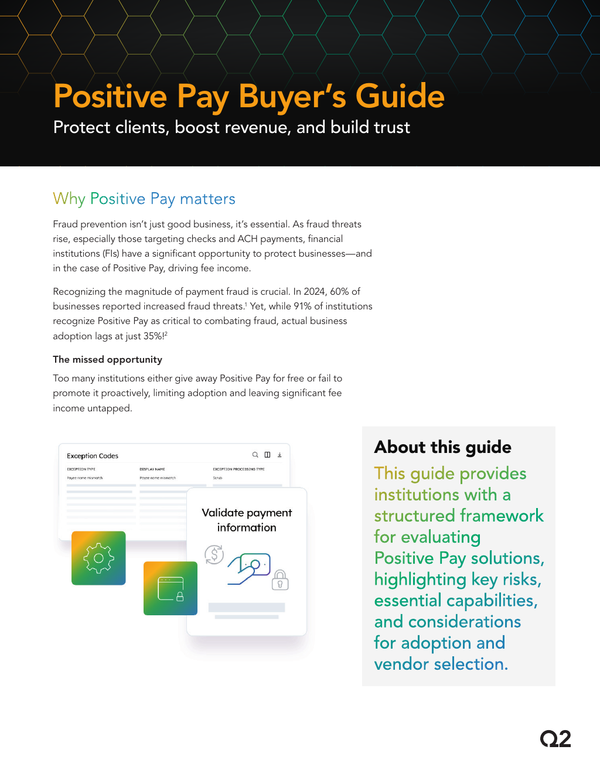

Positive Pay Buyer's Guide

Featured

Inside Gen Z: A Fintech Playbook That Works

Featured

Content types

None

Product Collateral

(3)

Podcast

(3)

Webinar

(2)

Market Analysis

(1)

White Paper

(1)

Topics

None

Fintech partnerships

(5)

Digital Banking

(6)

Personalization

(2)

Fraud

(3)

AI

(1)

Commercial Pricing

(1)

Segment

None

Small Business

(5)

Commercial

(5)

Consumer

(6)

Solutions

None

Fintech Integration

(4)

Digital Banking Platform

(6)

Targeting and Marketing

(2)

Risk and Fraud

(3)

Relationship Pricing

(1)