Schedule a Demo

Schedule a Demo

Read More

Content

Filter

10 results found

Featured

Unlocking Opportunity Across Your Small Business Portfolio

Featured

The M&A Tech Conversion Playbook: Steps and Considerations to Shape Long-Term Value

Featured

CFO Letter: Q1 2026

Featured

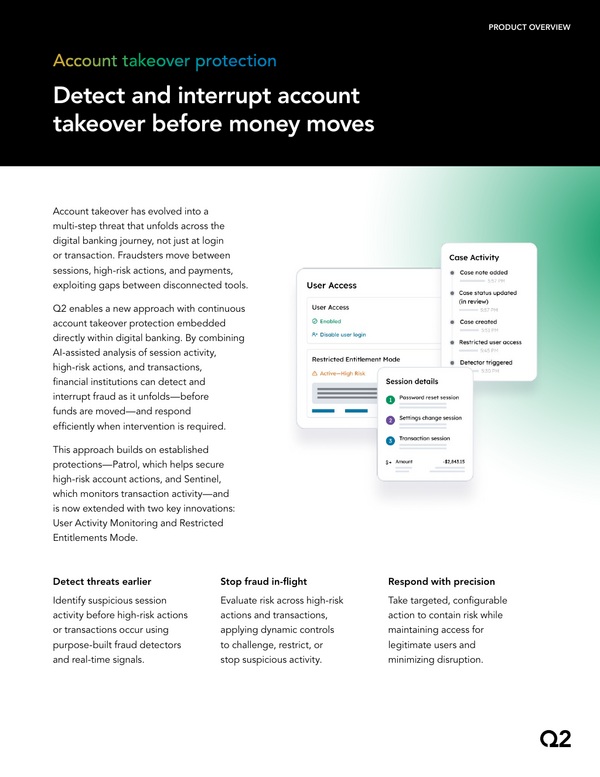

Account Takeover Protection Product Overview

Featured

Q2 Code Product Overview

Featured

Why Discipline, Not Momentum, Drives Better Bank Performance

Featured

Benchmark Your 2026 Strategies

Featured

Bank M&A Beyond the Balance Sheet

Featured

Nuvision Credit Union Case Study

Featured

What Bank Leaders Need to Know About Stablecoins

Featured

Content types

None

Webinar

(3)

Product Collateral

(2)

Podcast

(3)

Topics

None

Fintech partnerships

(3)

Digital Banking

(5)

AI

(1)

Commercial Pricing

(1)

Money Movement

(1)

Segment

None

Small Business

(5)

Commercial

(5)

Consumer

(6)

Solutions

None

Fintech Integration

(3)

Digital Banking Platform

(5)

Relationship Pricing

(1)

Payments

(1)