Schedule a Demo

Schedule a Demo

Read More

Content

Filter

10 results found

Featured

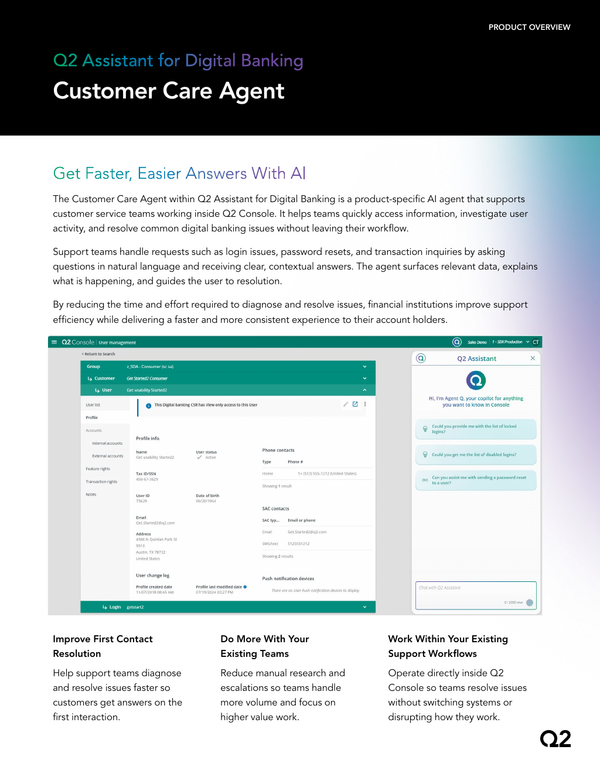

Customer Care Agent

Featured

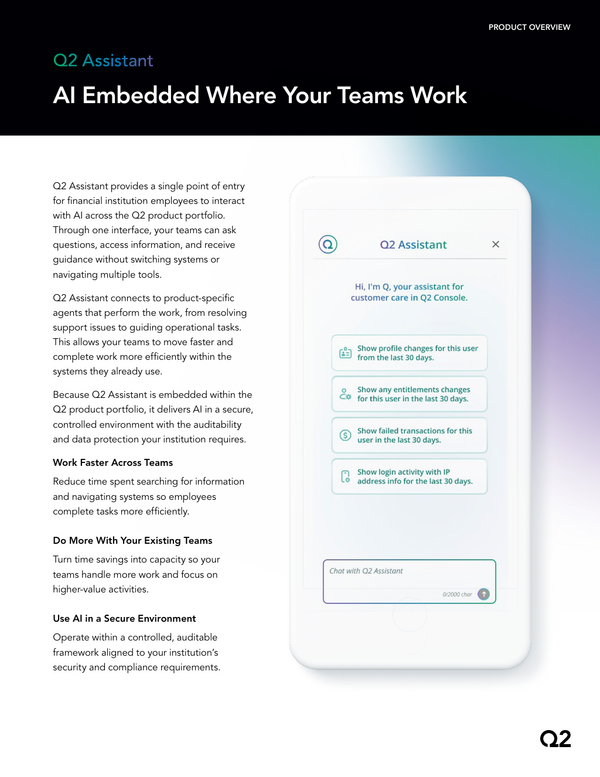

Q2 Assistant

Featured

The Hidden Cost of Banking Heroics

Featured

Innovation Playbook: Six Steps to Building Successful Fintech Partnerships

Featured

2026 Retail Banking Trends and Priorities: Credit Union Spotlight

Featured

Beyond Pricing Playbook

Featured

Unlocking Opportunity Across Your Small Business Portfolio

Featured

The M&A Tech Conversion Playbook: Steps and Considerations to Shape Long-Term Value

Featured

More Than Another AI Conversation

Featured

CFO Letter: Q1 2026

Featured

Content types

None

Product Collateral

(2)

Podcast

(2)

Infographic

(1)

Market Analysis

(1)

White Paper

(1)

Webinar

(2)

Topics

None

Digital Banking

(4)

Commercial Pricing

(2)

Fintech partnerships

(2)

AI

(1)

Segment

None

Small Business

(6)

Commercial

(7)

Consumer

(6)

Solutions

None

Digital Banking Platform

(4)

Relationship Pricing

(2)

Fintech Integration

(2)