Schedule a Demo

Schedule a Demo

Read More

Content

Filter

10 results found

Featured

Positive Pay Adoption Playbook

Featured

Javelin 2025 Small Business Digital Banking Vendor Scorecard

Featured

Q2 Customers on Turning Digital Into a Differentiator

Featured

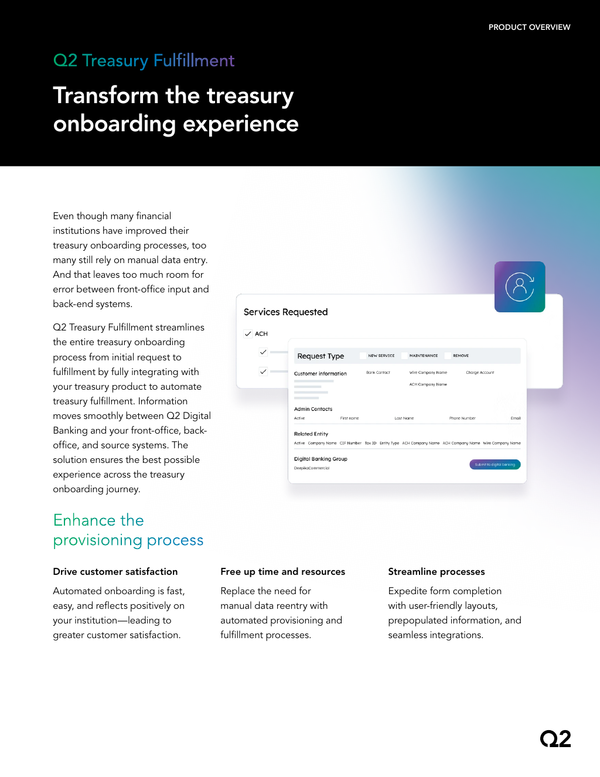

Treasury Fulfillment Product Overview

Featured

Unclogging the Bottleneck of Treasury Onboarding

Featured

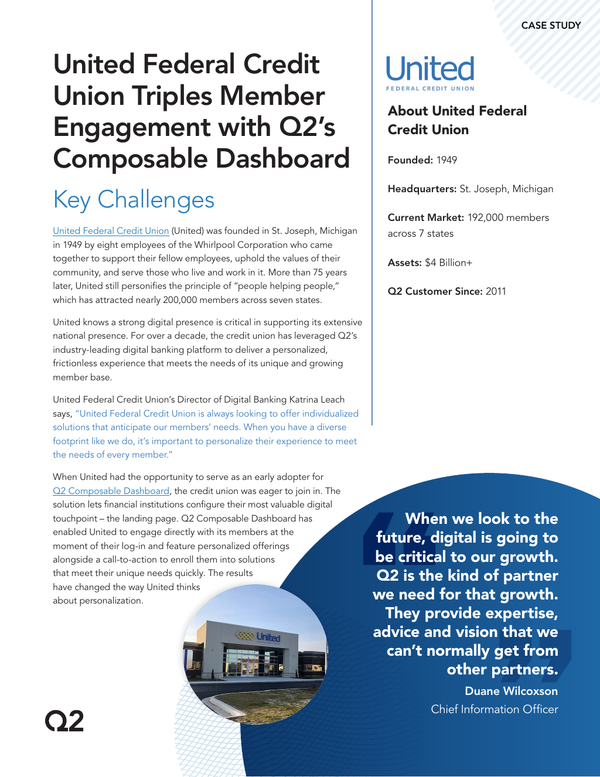

United Federal Credit Union Triples Member Engagement With Q2’s Composable Dashboard

Featured

Commercial Loan and Deposit Pricing Market Update: August 2025

Featured

Q2 Business Overview

Featured

Building Digital Banking Trust With Tech-Driven Dispute Management

Featured

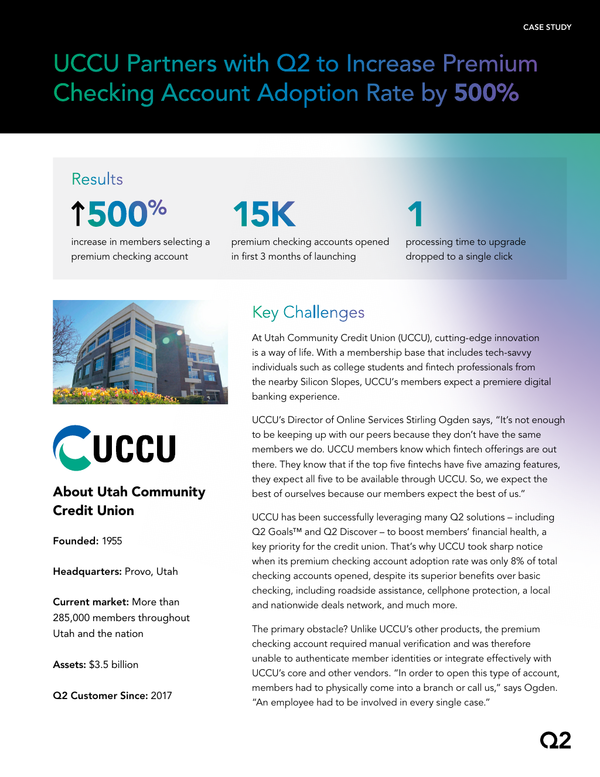

UCCU Partners With Q2 to Increase Premium Checking Account Adoption Rate by 500%

Featured

Content types

None

White Paper

(1)

Market Analysis

(1)

Blog

(3)

Product Collateral

(1)

Podcast

(1)

Case Study

(2)

Infographic

(1)

Topics

None

Positive Pay

(1)

Fraud

(2)

Digital Banking

(5)

Fintech partnerships

(1)

Personalization

(1)

Money Movement

(2)

Segment

None

Commercial

(6)

Small Business

(5)

Consumer

(4)

Solutions

None

Risk and Fraud

(2)

Digital Banking Platform

(5)

Fintech Integration

(1)

Digital Onboarding

(3)

Payments

(2)

Relationship Pricing

(2)