Commercial Loan and Deposit Pricing Market Update: November 2024

This month’s analysis looked at how the commercial loan pricing and deposit market responded to the Fed rate cut in mid-September and what that might tell us about what's to come after the additional rate cut in early November.

In particular, we looked at the funding curve's movement toward a more familiar slope, and how that's impacting pricing for fixed-rate loans, as well as deposits.

Read on to get more details.

Data Notes:

• This market update is based on the previous month’s (October 2024) data in the Q2 PrecisionLender database.

• Q2 PrecisionLender uses an assumed marginal duration matched funding cost, not the bank’s actual average cost of funds, when referring to the Cost of Funds (COF) on loan pricing activity.

• We define Regional+ as institutions with $8B+ in assets, while Community are <$8B.

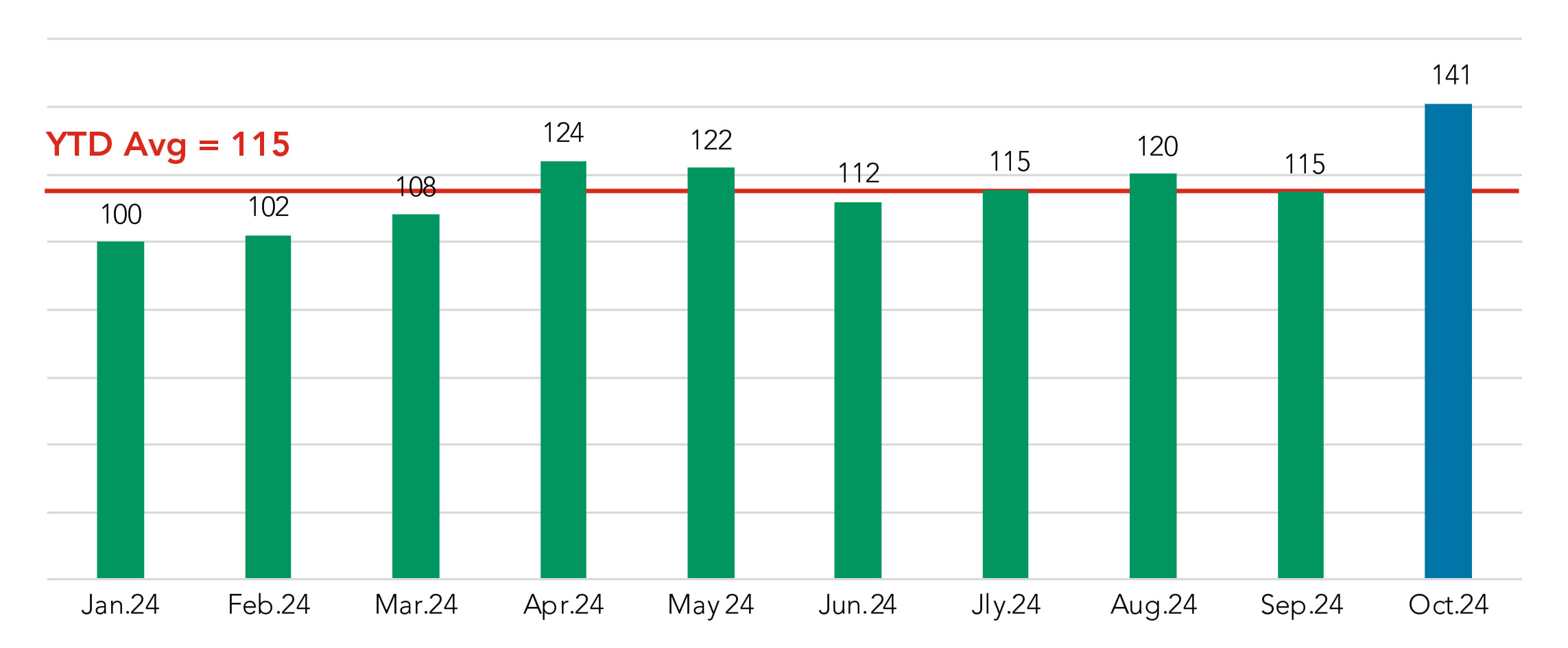

Pricing volume spikes upward

Pricing volume made a significant increase in October. The 22% month-over-month increase was the largest since another 22% jump, from February to March 2023. While the 50 bps drop in the Fed rate in September likely sparked borrowers’ interest in exploring new deals, we checked the database to be certain. We found the increase was driven in part by an uptick in average deals per banker and also by a greater number of bankers pricing deals during October.

Priced Commercial Loan Volume in $

Indexed to January 2024 = 100

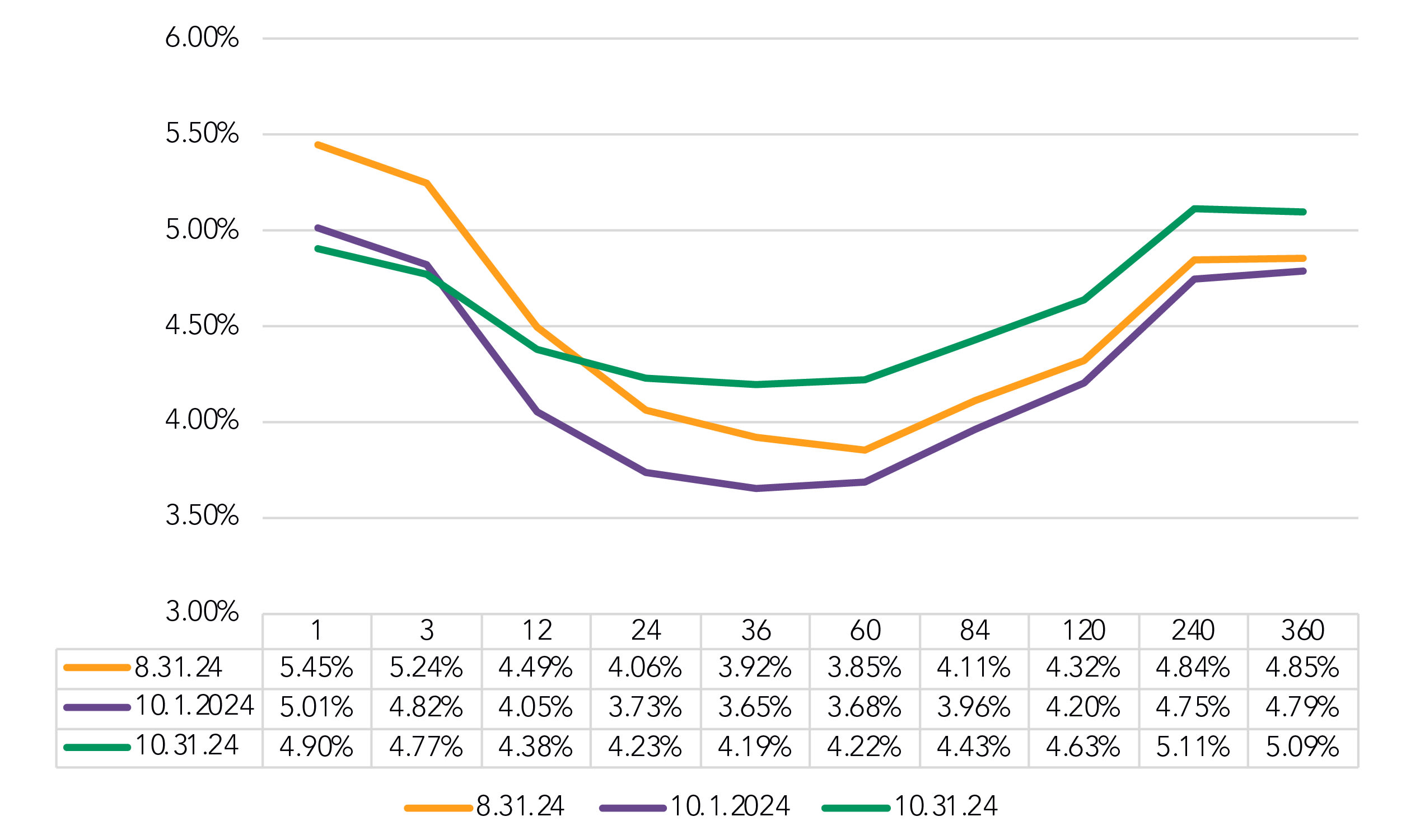

FHLB curve moves closer to traditional slope

In the aftermath of the September Fed rate cut, market rates went the opposite direction, for 12-month terms and beyond. The 60-month rate rose 54 bps from Oct. 1 to Oct. 31.

At the time of this writing the increases have continued into November, with the 60-month benchmark rising an additional 20 bps from the Oct. 31 benchmark to Nov. 7.

FHLB Curve

Selected Dates

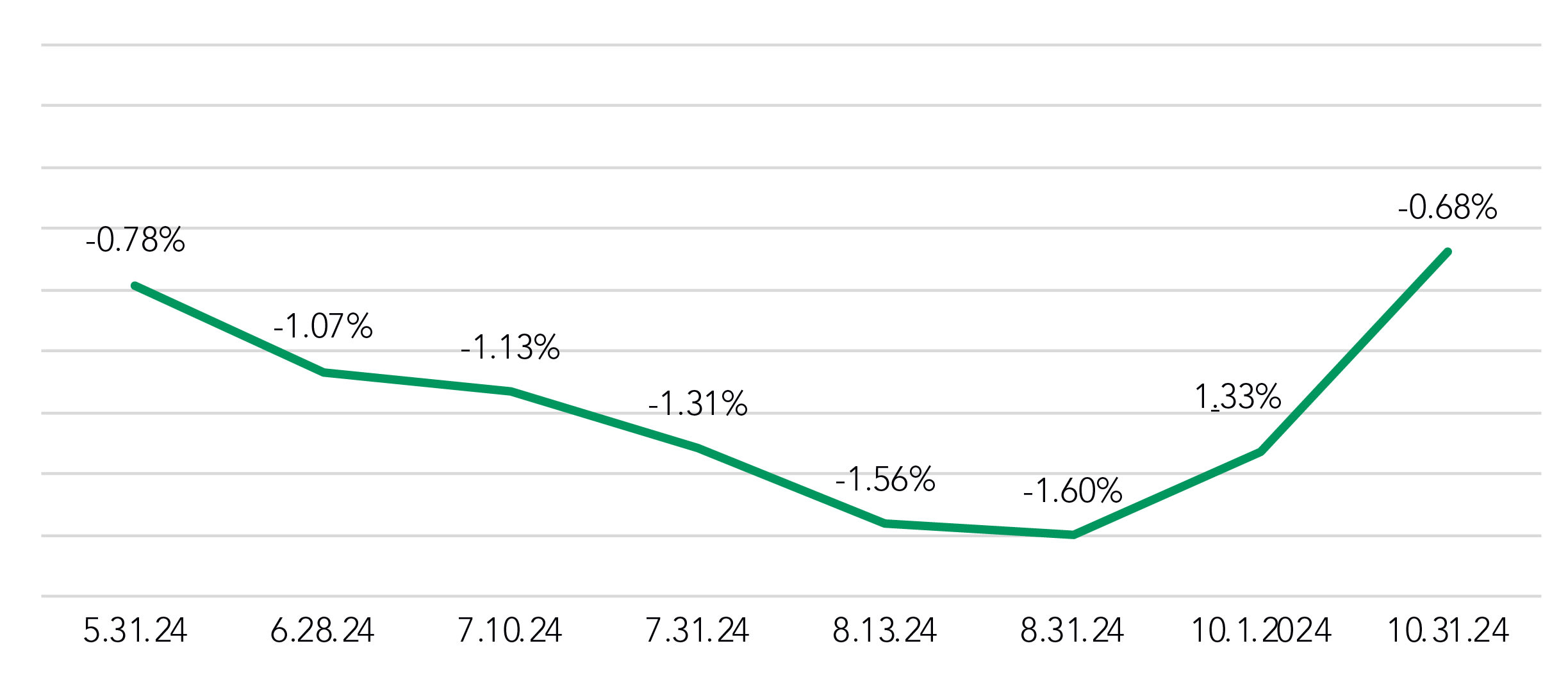

The result is the shallowest inversion, a -.68% carry from 1 month to 60 months, since October 2023—and the second shallowest since the curve inverted in November 2022.

FHLB Carry

1 Month to 60 Months

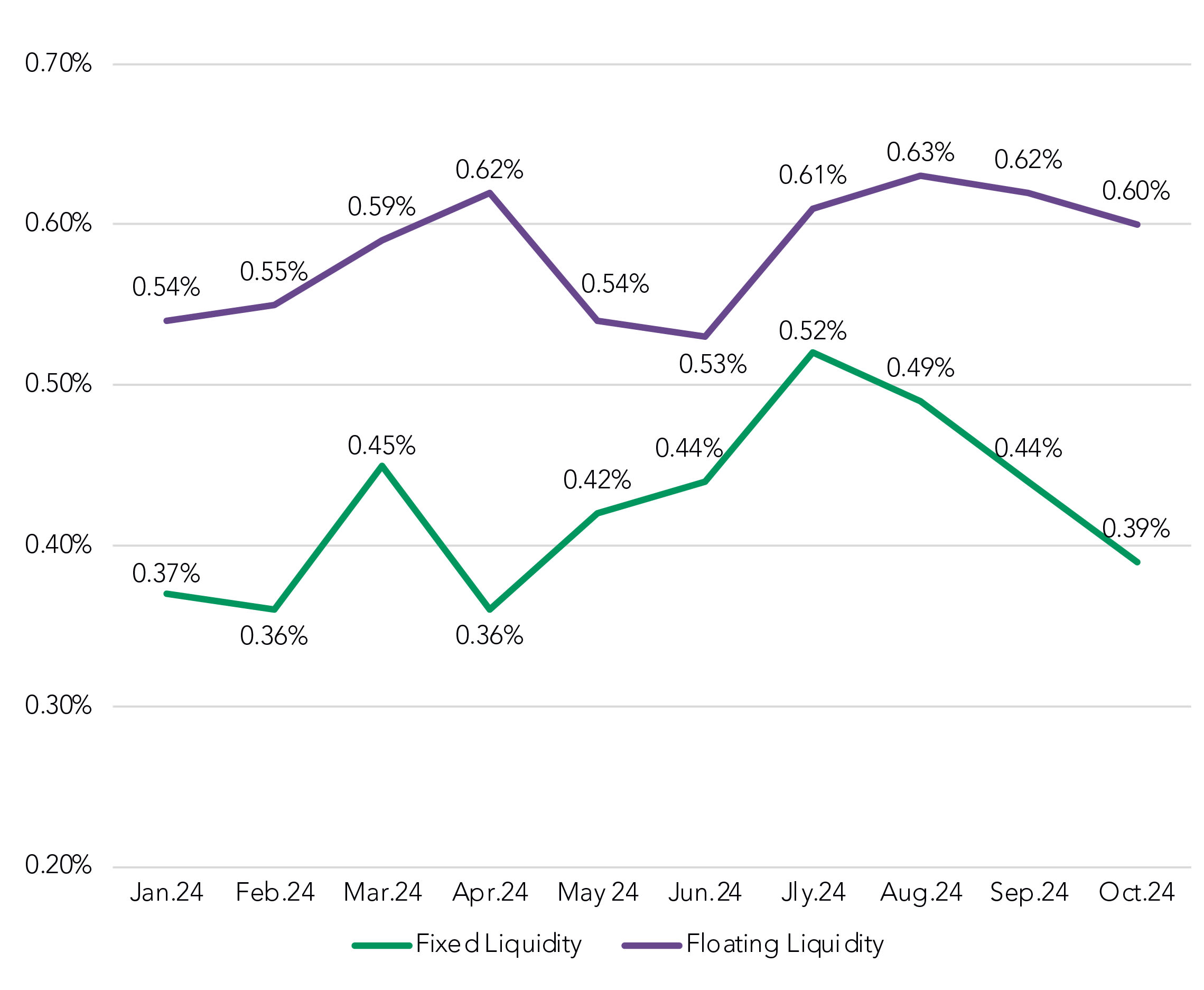

Liquidity costs drop as market rates rise

As the market rates have risen, banker liquidity adjustments have dropped accordingly for fixed-rate loans. October marked the third straight month-over-month drop, down 13 bps since July. Liquidity adjustments for floating rate loans (average maturity ~39 months) have moved in a narrow range of ~60 bps over the past four months.

Approximate Liquidity Cost

Rolling Trend

Amid rising market rates, deposit rates remain static

In the immediate aftermath of the Fed cut in September, we saw a modest drop in deposit rates. But with rising market rates in October, deposit rates essentially remained unchanged.

The previous “rule of thumb” was that deposit pricing managers would drop their rates with the goal of mirroring Fed rate cuts. But that no longer appears to apply in this current environment. A low unemployment and high business activity could generate an increased need for liquidity, and with the liquidity crisis only recently in the rearview mirror, banks may be willing for now to keep paying higher deposit rates.

We’ll check in again on this metric in future updates to see how deposit rates respond to the November fed rate drop.

Note: Deposit rate paid information is from portfolio snapshots sent from institutions throughout the month and is not a single month-end view.

Overall Deposit Rate Paid

Includes NIB Base

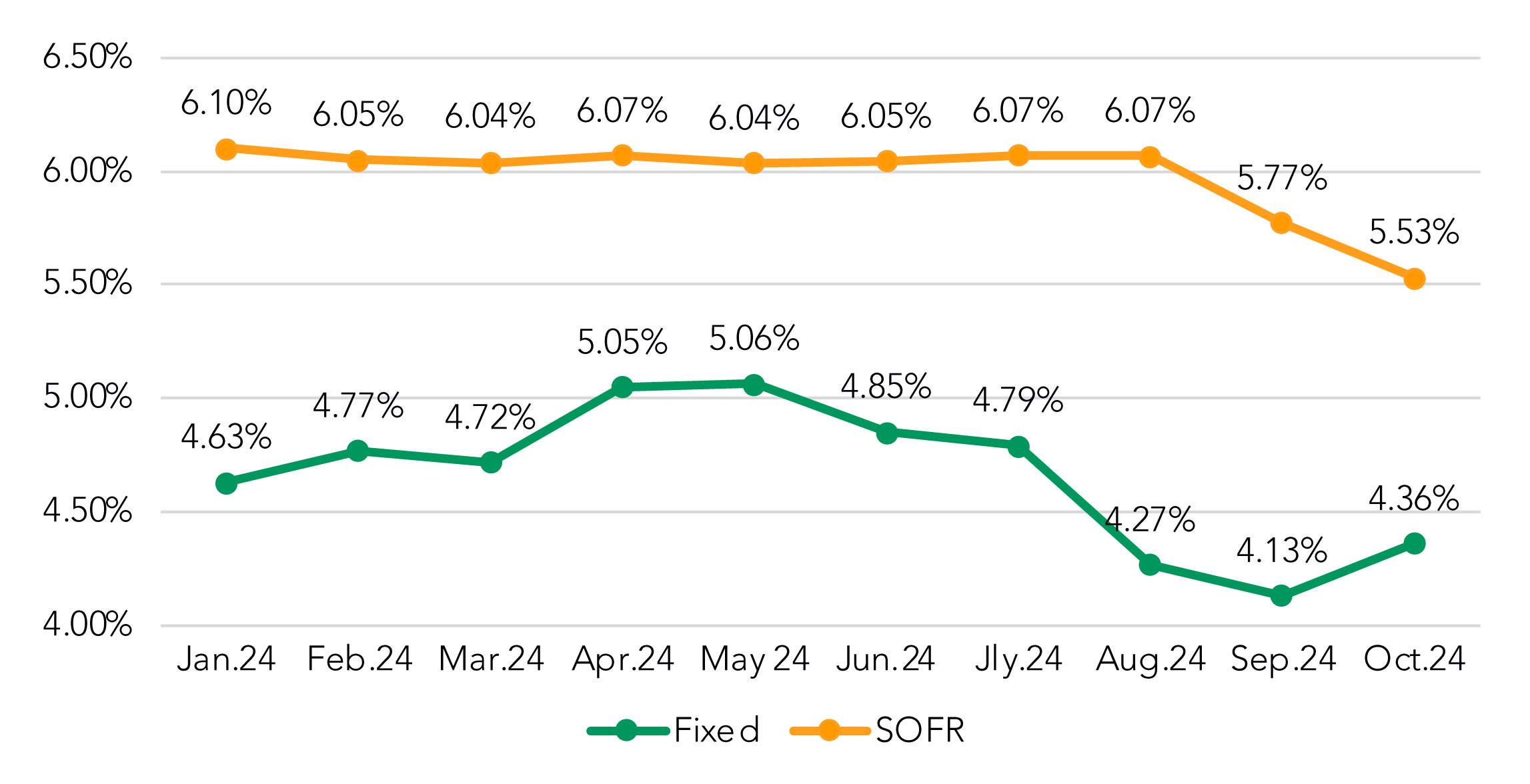

COF gap closes between floating and fixed rates

A full month of data post the mid-September Fed rate drop meant that all-in COF on floating rates completed their ~50 bps drop from August. (6.07% down to 5.53%). Meanwhile, as noted above, rising market interest rates pushed up fixed-rate all-in COF by 23 bps to 4.36%.

The gap between the two metrics in October was 1.17%, the closest they have been since May.

All-In COF by Month

Rolling Trend

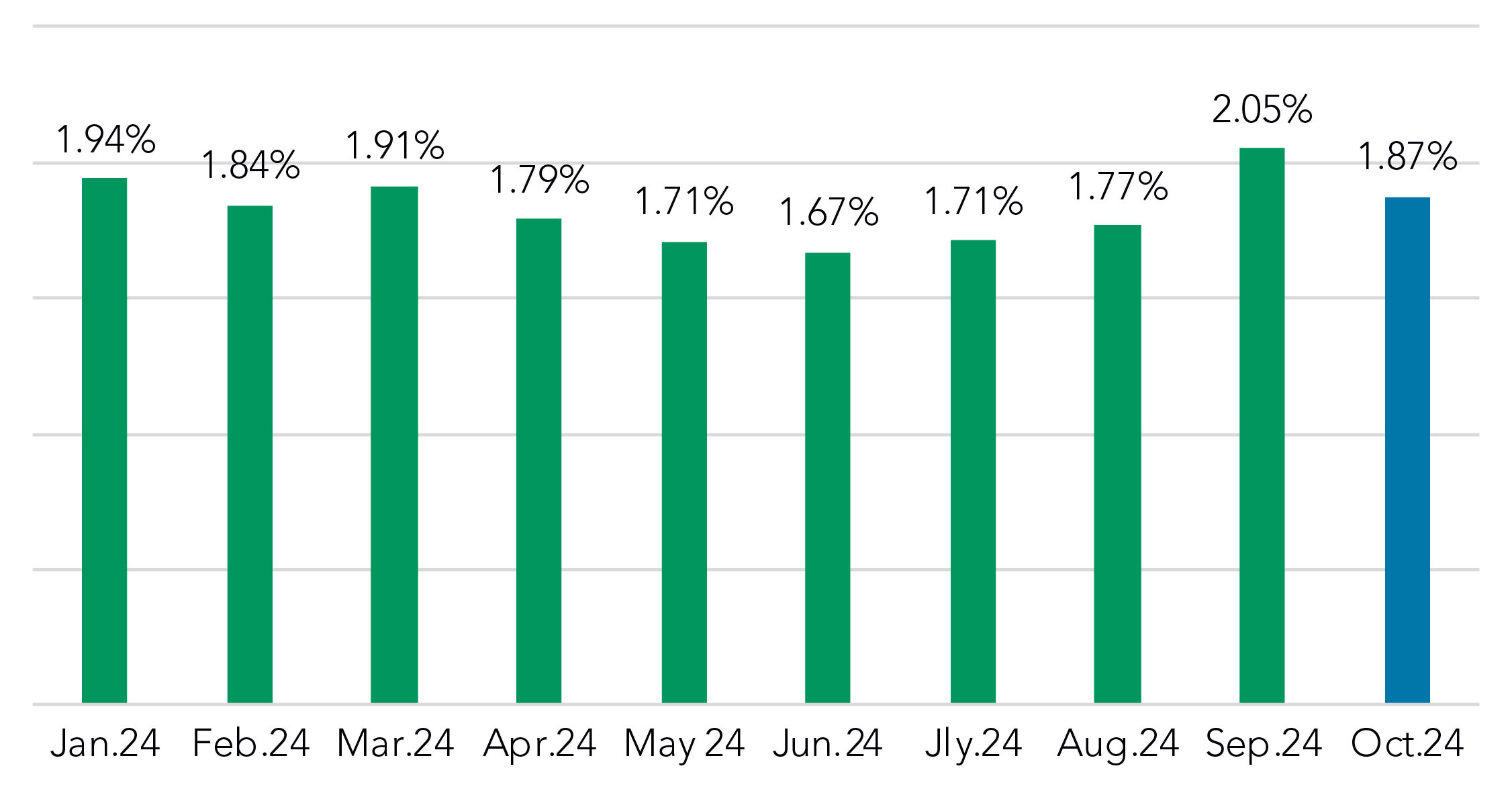

Fixed-rate spreads can’t keep up with rising rates

After adding 28 bps in fixed spreads in September, bankers gave back 18 in October (dropping from 2.05% to 1.87%).

Fixed-Rate Coupon Over COF Rate

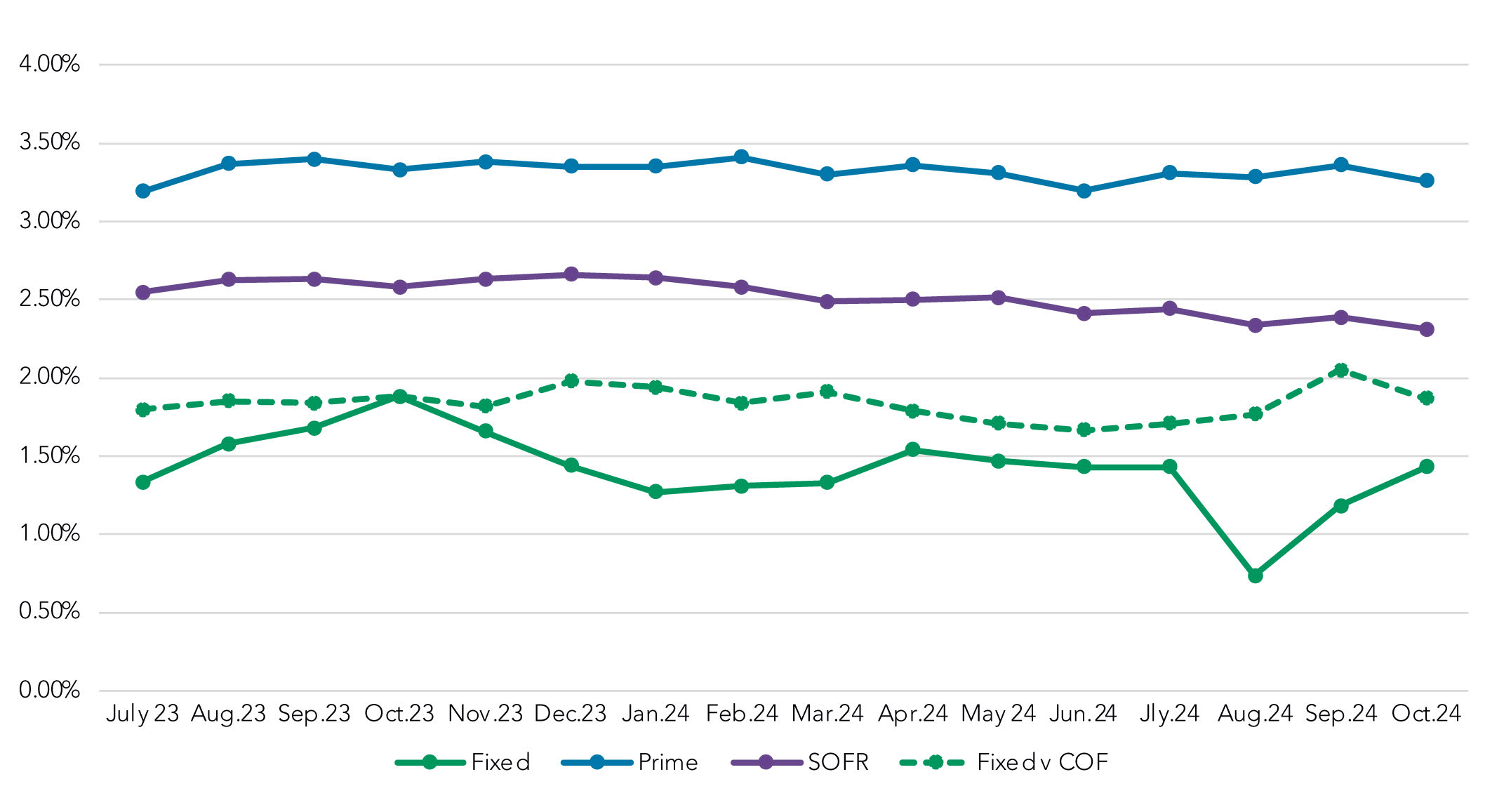

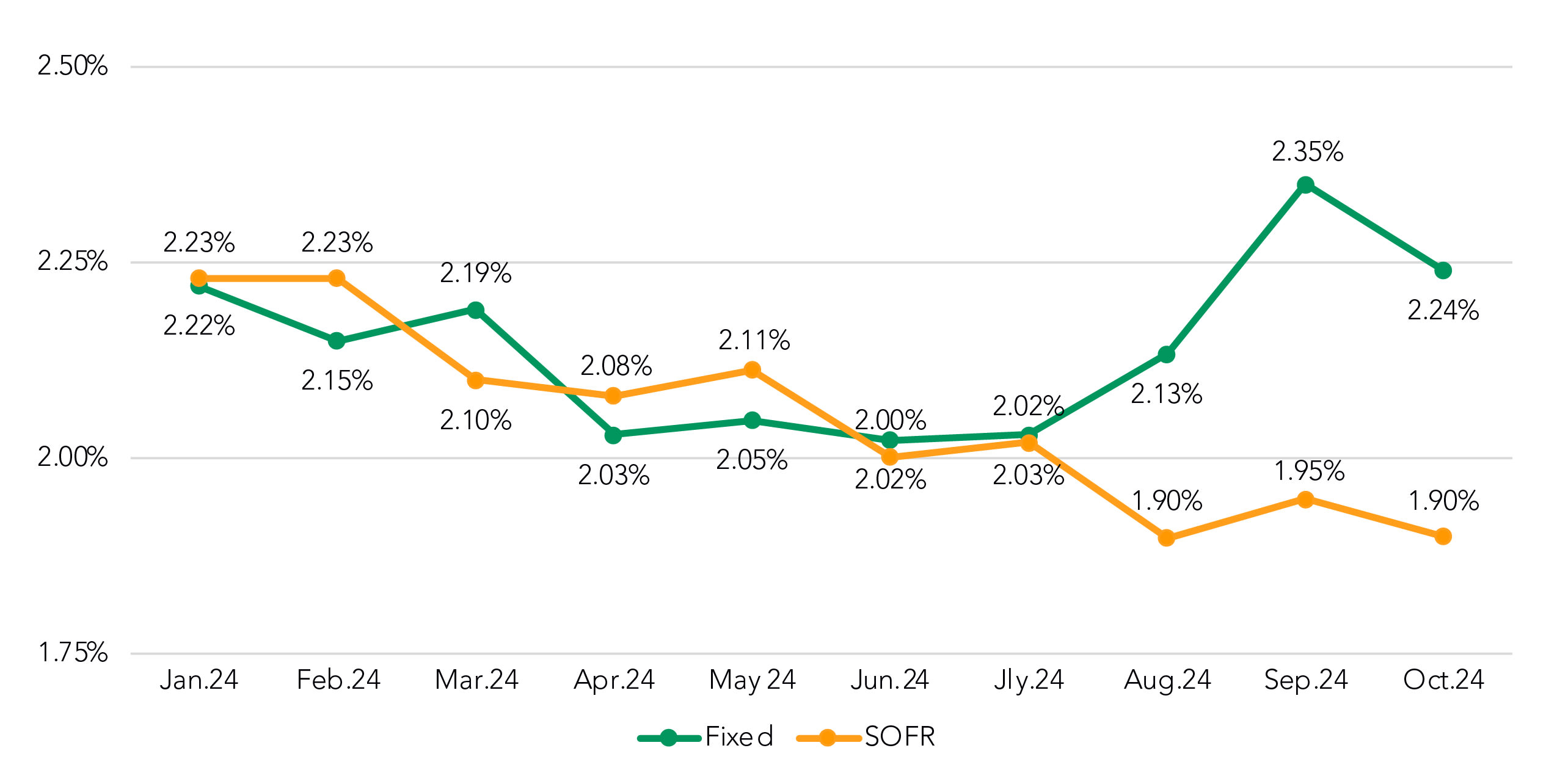

Note: We’ve received diverging feedback from bankers about which way they prefer to see fixed-rate spreads displayed. Some prefer the chart above, which expresses it in the straightforward context of fixed-rate COF. But others prefer to see fixed-rate spreads in the chart below, which uses the SOFR equivalent a comparison of different structure types. In this view, it is clear that the relative “discount” fixed-rate loans compared to SOFR structures has narrowed since August.

SOFR Equivalent Spread by Structure Type

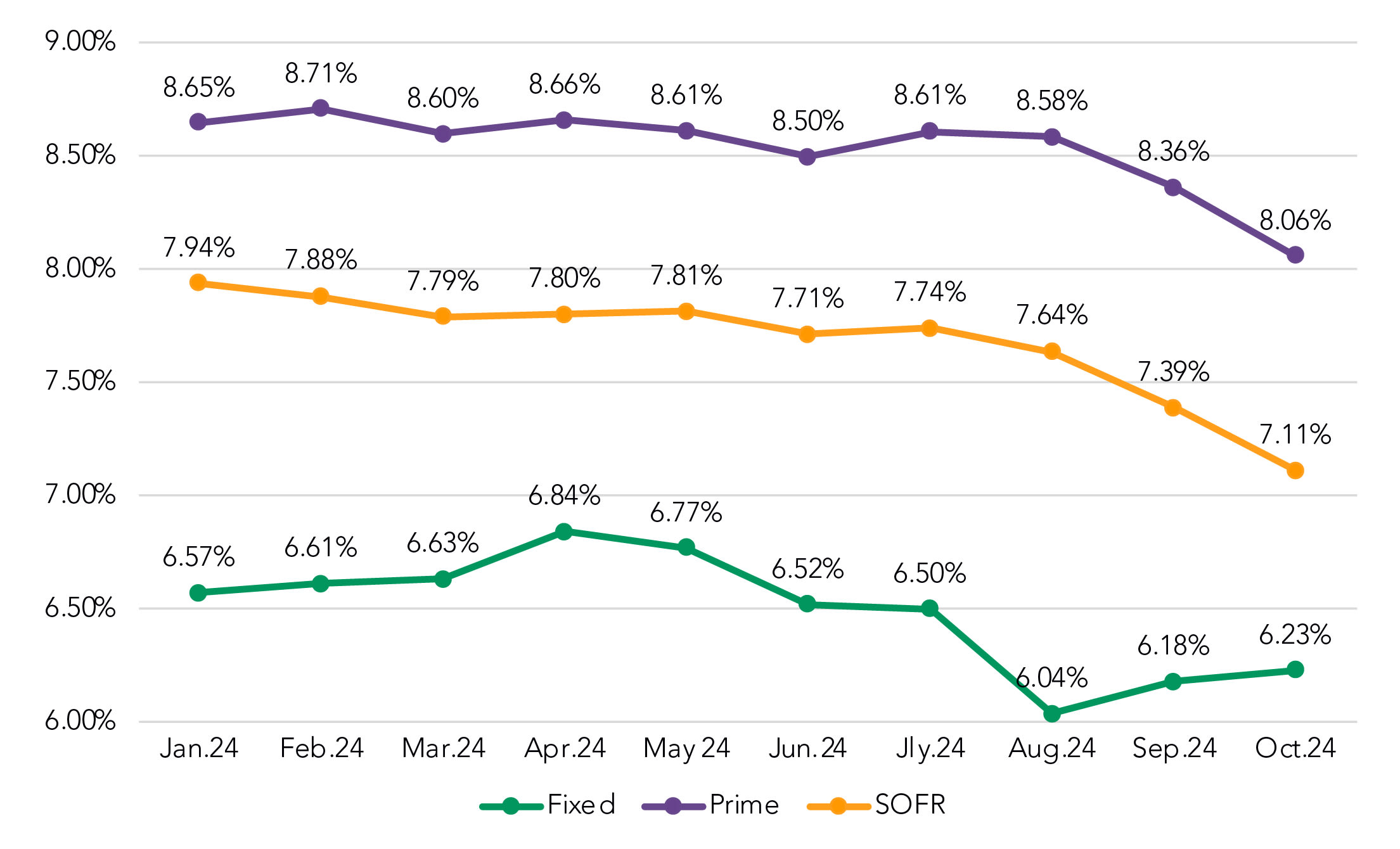

Fixed coupon rises slightly; floating coupons mirror Fed cuts

The drop in fixed-rate spreads meant that fixed-rate coupons rose only modestly in October (from 6.18% to 6.23%) despite the previously noted increase in funding costs.

Meanwhile, static floating rate spreads meant that floating rate coupons essentially mirrored funding costs, dropping ~50 bps from August to October for both Prime- and SOFR-based structures.

Coupon Rate by Month

Rolling Trend

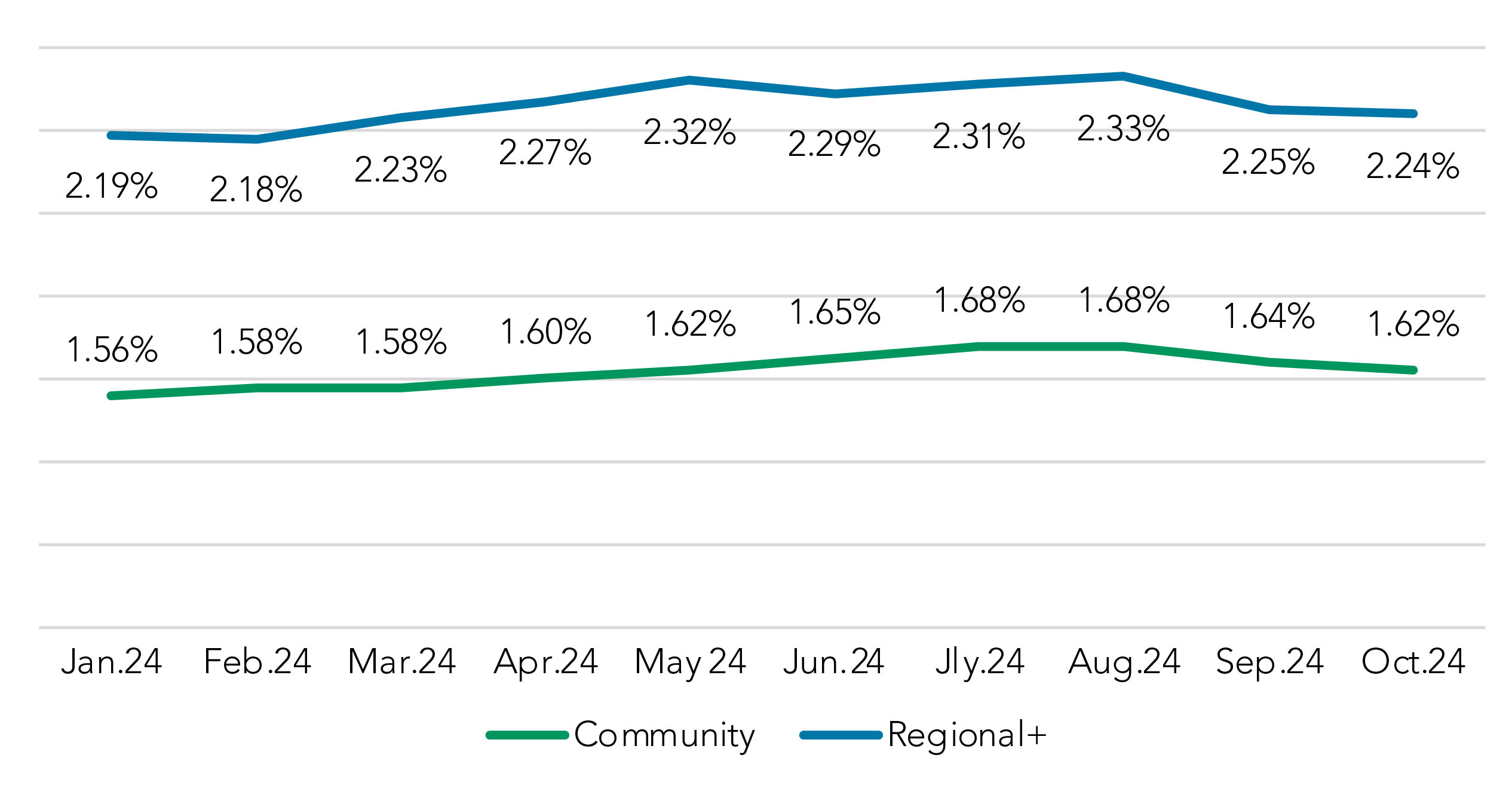

Fixed-rate NIM drops

It all netted out to an 11 bps drop in fixed-rate NIM, after having added 33 bps over the previous two months. Meanwhile, SOFR NIM was unchanged over the same time period, but remains 33 bps below its January 2024 mark.

NIM by Month

Rolling Trend

Got questions?

Our banking consultants and data scientists are combing through Q2 PrecisionLender pricing data every day. If there is anything you’d like to know about what they’re seeing, please send your questions to insights@q2.com.